The Lobito Corridor - seeking synergies between the Global North and Africa

- For the European Union and the US, the Lobito transport corridor—a network of rail links leading to the port of Lobito in Angola—is the flagship infrastructural project in Africa.

- The corridor is intended to streamline exports to the EU and the US of raw materials essential for the development of new technologies, particularly copper and cobalt from the Democratic Republic of the Congo (DRC), and in future also from Zambia.

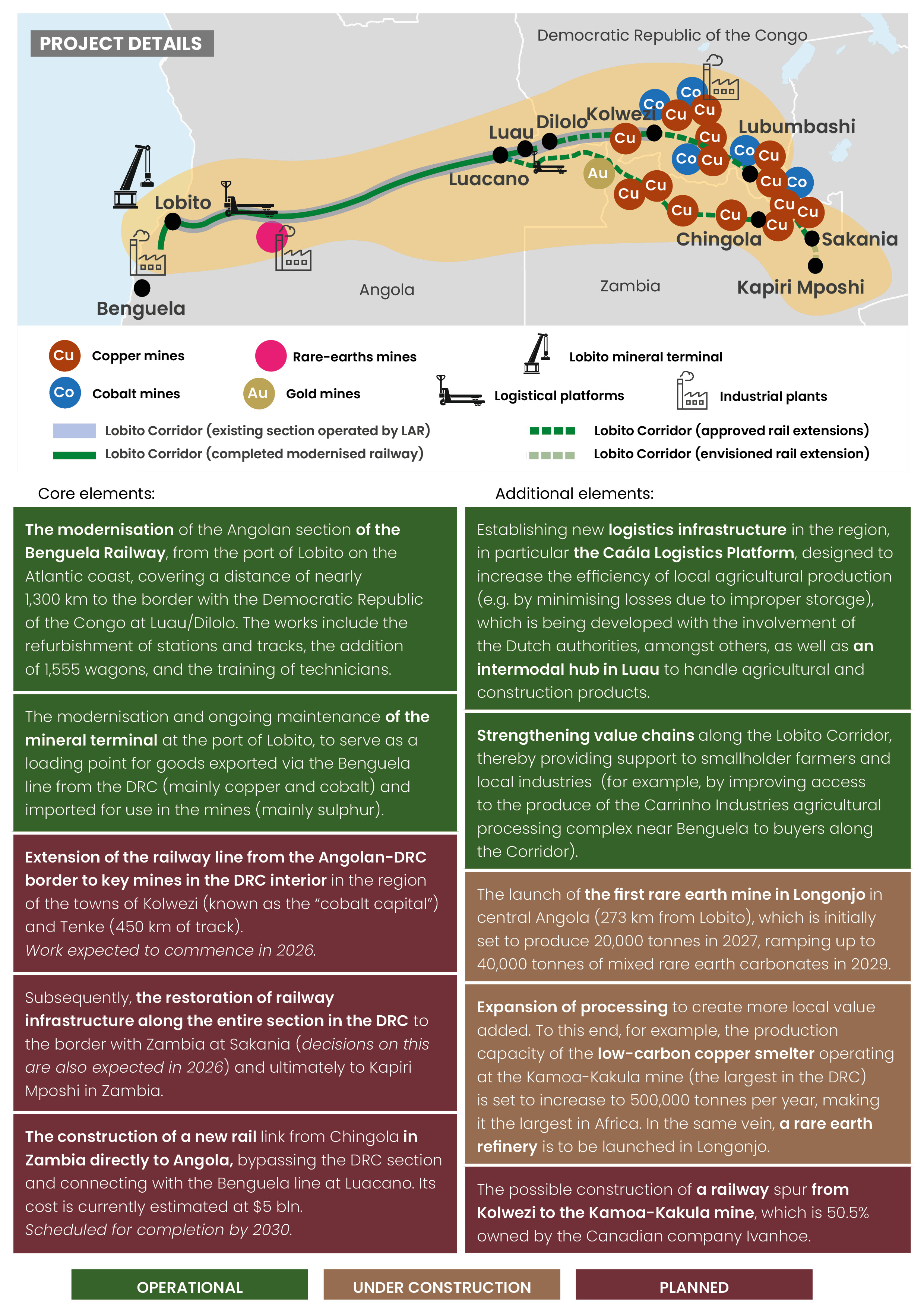

- A railway line between the port of Lobito and Angola’s border with the DRC, with a road extension into the DRC’s Kolwezi, is already operational. Plans are at an advanced stage for the reconstruction of the railway in the DRC between the borders with Angola and Zambia, and for the construction of a new link from Zambia directly to Angola.

- The region – rich in raw materials – is the subject of intensifying competition among global powers. Therefore, the sustainable nature of the project is intended to serve as an example that cooperation with the West can be more beneficial than with China.

- Despite progress in implementing the project, the benefits for the participating African countries remain limited for the time being. This is due to differences in interests and the scale of commitment among the partners. Consequently, it is difficult to regard the overall success of this investment as certain at present.

- From the perspective of African nations, the success of the project’s subsequent phases will be closely linked to meeting their development expectations, along with respecting their aspirations to gain greater control and decision-making power over the use of their natural resources.

- For the EU, it will be crucial to maintain its image as a reliable and supportive partner for these aspirations. Against this backdrop, differences with the US are becoming increasingly apparent, offering an opportunity which the EU may turn to its advantage.

Sven Torfinn / Panos Pictures / Forum

Sven Torfinn / Panos Pictures / Forum

The Origins of the Lobito Corridor

Although the idea of the Lobito Corridor – a transport network extending to the port of Lobito in Angola – is not new, the project in its current form emerged against the backdrop of developed nations’ growing need for access to critical minerals essential for technological transformation. The International Energy Agency estimates that global demand for minerals such as lithium and nickel will increase by a factor of several dozen between 2020 and 2040. Central and Southern Africa are among the world’s most important sources of these minerals (for example, 26 of the 51 most sought-after minerals are found in Angola). Copper will also play a key role in the energy transition, and the largest deposits and mines are located in the DRC and Zambia. The latter plans to produce 1 million tonnes of copper in 2026 and aims to triple this volume by 2031.[1] In turn, the DRC is home to 80% of the world’s cobalt deposits, whilst 73% of global cobalt production is located in the Congolese provinces of Lualaba and Haut-Katanga.[2]

Western countries have long sought to present an alternative to China’s Belt and Road Initiative in the field of global connectivity infrastructure. To this end, at their summit in June 2022, the G7 members (the US, Japan, Germany, the UK, France, Italy and Canada) established the Partnership for Global Infrastructure and Investment (PGII). This initiative was intended to mobilise $600 billion by 2027 to create infrastructure supporting sustainable development in developing countries. The US International Development Finance Corporation (DFC)[3] was to play a key role in this.

The establishment of the PGII coincided with a major infrastructure agreement in July 2022. The Angolan authorities awarded a 30-year concession to the largely European Lobito Atlantic Railway (LAR) consortium to operate both the mineral terminal at the port of Lobito and the neglected Benguela Railway (Caminho de Ferro de Benguela, CFB) connecting the port to the DRC border. The extension of this route reaches mines in the provinces of Lualaba and Haut-Katanga in the DRC and the Copperbelt in Zambia. The consortium consists of Western firms, including the Portuguese Mota-Engil, the Belgian Vecturis, and Trafigura, a commodities trading giant with offices in Singapore and Switzerland. Significantly, the tender was won by the LAR consortium, beating out Chinese competitors. This is notable given that Chinese entities had previously rebuilt the civil war-ravaged Benguela line for $1.8 billion between 2006 and 2014, while until 2013 the Chinese company CCCC had also overseen the expansion of Lobito port.

In May 2023, then-President Joe Biden announced that, as part of the PGII, the US would focus on developing “transformative economic corridors” in the Global South.[4] Among the key projects selected for implementation was a plan to upgrade and expand the infrastructure around the Benguela railway in Angola. Its aim was not only to speed up the transport of minerals extracted in Zambia and the DRC (particularly copper and cobalt, but also zinc and lithium), but also to substantially increase export volumes via the expanded port of Lobito. The region’s countries stood to gain new development opportunities as a result of the expected boost to internal transport (primarily in Angola[5]), passenger traffic and trade between Zambia, the DRC and Angola, as well as the facilitation of exports of non-mineral products, such as agricultural goods.

Stakeholders Involved

From the outset, the project has been based on cooperation and a division of roles between the US and the European Union (EU). Since 2022, the EU and the US have been linked by the Mineral Security Partnership (MSP), a strategic intergovernmental agreement involving, amongst others, Japan, Australia and South Korea.[6] In September 2023, when the EU joined the PGII, both entities announced their cooperation as key partners for developing the Corridor and declared their support for the governments of the three countries in the region in the pre-feasibility work on the new Angola–Zambia railway line.[7] In turn, in October 2023, the EU and the US reached an agreement to cooperate on the Lobito Corridor based on a “shared vision.”[8] They partnered with the governments of Angola, Zambia and the DRC, as well as the African Development Bank (AfDB). The agreement also includes the Africa Finance Corporation (a financial institution for African countries and enterprises supporting infrastructure), which acts as the overall developer of the line[9] and operationalises DFC funds. Although LAR is a predominantly European consortium, it sought financing for its projects primarily from American sources – for example, in November 2025, it secured funding from the DFC (US $553 million). In 2025, experts from the US and the EU jointly conducted feasibility studies for the Congolese section, and the US government lobbied for the Portuguese firm Mota-Engil to be awarded the concession to modernise and manage the route to the DRC-Zambia border, which forms an extension of the LAR line and will also be financed by the DFC.[10]

The Corridor is a top priority for both the US (which has so far allocated around $4.5 billion in private and public funds to the project[11]) and the EU (which had contributed a total of around €2 billion at the end of 2025[12]). Its importance is evidenced by its status as a flagship project both under the PGII[13] and EU Global Gateway initiatives.

The EU is involved in the Lobito Corridor as part of Team Europe for the Lobito Corridor, which also includes the European Investment Bank, Belgium, the Czech Republic, France, Spain, the Netherlands, Germany, Portugal, Sweden, Italy, and several national development agencies and private sector companies.

Among the financial backers, the United Kingdom also plays an important role (having provided €415 million through UK Export Finance), as does the World Bank (with the DRC applying for a $500 million loan regarding the Congolese section of the railway in October 2025). Italy considers its participation in the Lobito Corridor project to be part of the Mattei Plan for Africa.

For the three African countries where the projects are being implemented, since January 2023, the primary framework for cooperation in this area has been the Lobito Corridor Transit Transport Facilitation Agency (LCTTFA) Agreement. The Southern African region, where South Africa plays a leading role, is participating in the project through the involvement of the Development Bank of Southern Africa (DBSA) (e.g. $200 million in LAR co-financing). Other countries have also expressed a desire to join the project, such as Egypt, which has been seeking to involve its domestic companies in Corridor investments since late 2025.

Competition and Rivalry among Great and Emerging Powers in the Region

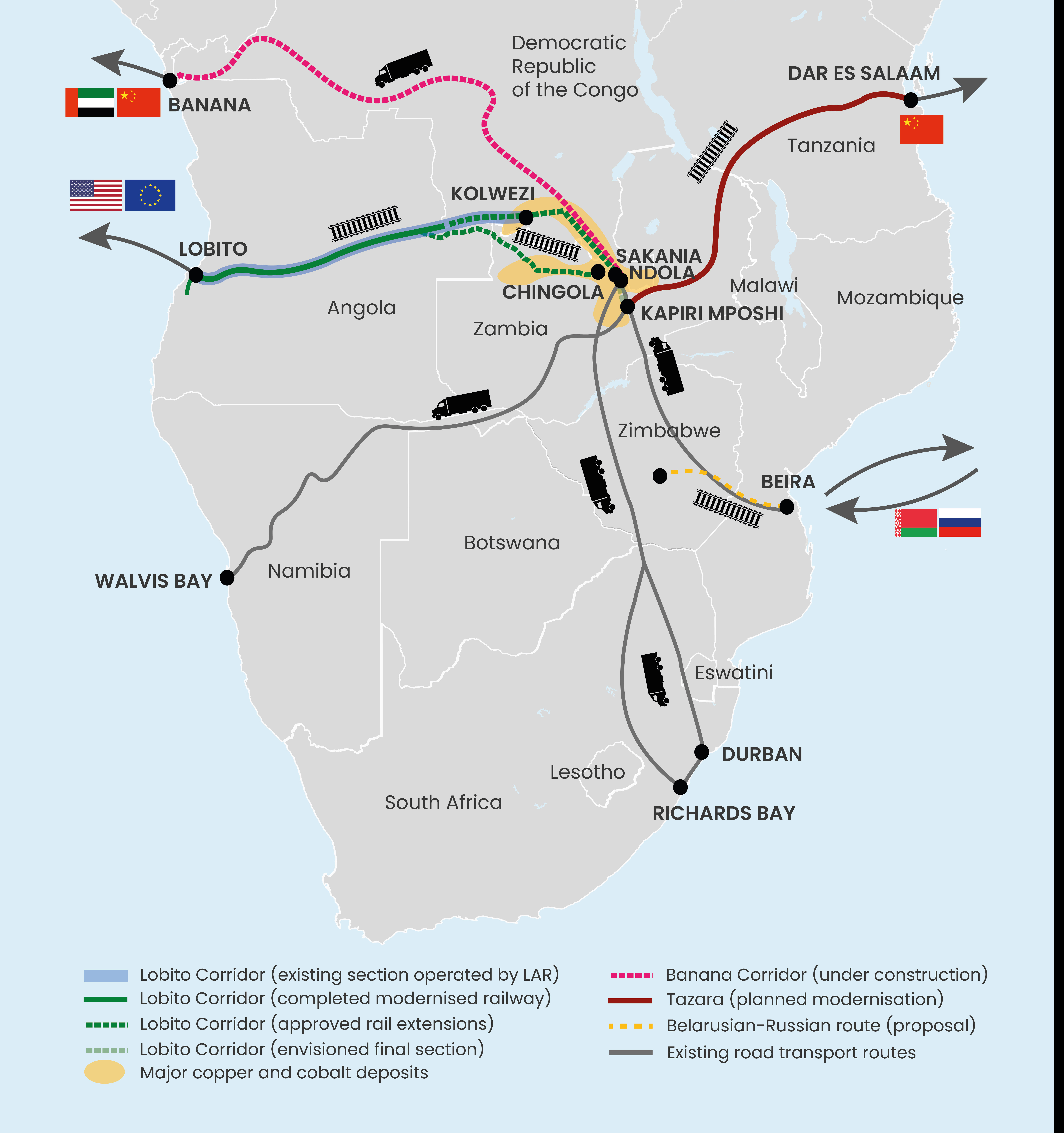

From the beginning of the 21st century, China has been the main lender in Africa, having granted approximately $160 billion in loans between 2000 and 2022, with Angola receiving the largest share (approximately $45 billion). Its position as the partner of choice in the field of infrastructure development in Africa has so far remained unshaken. Chinese entities also dominate the mining sector, controlling 80% of copper mines in the DRC. The situation is similar regarding rare earth minerals: the Chinese control, either wholly or in part, 15 of the 19 cobalt mines in the DRC and are responsible for the extraction of 76% of raw material in the country.[14] Although the Lobito project is intended to weaken their position, Chinese entities are constantly expanding their investments in the region. For example, the lithium mine in Manono in the DRC, which the Chinese company Zijin plans to launch in 2026, is set to be one of the largest in the world.[15]

LAR’s success in winning the tender to operate the Benguela Railway was a rare example of a Western bid gaining the upper hand over a Chinese one in the infrastructure sector. Therefore, the project is intended not only to serve tangible economic and development objectives, but also to demonstrate the ability of Western nations to engage in such forms of cooperation with African—and, more broadly, developing—nations, showing the ability to compete against Chinese proposals. Consequently, unlike Chinese projects, which rely on workers, equipment and materials from China, 97% of the Lobito workforce on the Angolan section are Angolans. The involvement of the African industrial base is also emphasised; for example, a significant share of the railroad carriages is sourced from a South African manufacturer.[16]

At this stage, Europe and the US are capitalising on the Angolan authorities’ dissatisfaction with their Chinese partners on the Benguela Railway between 2006 and 2014, which left behind poor-quality infrastructure, incompatible computer equipment and unfulfilled promises to develop freight and passenger traffic.[17] Now, however, it is the actions of the Western consortium that will be scrutinised, and the assessment will be influenced by heightened expectations regarding tangible benefits for the countries involved. The Chinese side will be keen to see this experiment fail, hoping to defend its regional position and potentially reclaim the vacated space in the future. So far, China’s response to the project includes a commitment to modernise the railway link from Zambia to Tanzania (Tazara), so that minerals from Zambia can be transported in greater quantities to China via the port of Dar Es Salaam on the Indian Ocean coast. Once renovated, this line would return to its original capacity of 5 million tonnes of cargo.[18] There are also signs of work on (at least a declarative) adjustment to China’s approach to cooperation in Africa. During the G20 meeting in Johannesburg in November 2025 (shortly before the EU–African Union summit in Luanda), the Chinese authorities presented a new initiative for the modernisation of Africa. It emphasises a departure from the previous model, where China both acted as the sole initiator of projects and the exclusive implementer. This time, the greater involvement of African partners was highlighted. In this way, China hopes to send a signal that it has “learned its lesson,” and is ready to offer partnerships on terms more favourable to African countries. Despite losing its lead in the Lobito Corridor, China intends to make use of the infrastructure being built by LAR. This is evidenced, for example, by the transport bookings made on this line by Zijin[19] (which owns a 49.5% stake in Kamoa-Kakula).

Russia and Belarus are also interested in the region’s infrastructure – the latter is primarily present in Zimbabwe, which is an important market for its tractors as well as a source of gold. In February 2026, Alexander Lukashenka proposed a joint investment with Zimbabwe in a dry port in Mozambique (likely situated near the cities of Beira or Nacala, locations in which he has previously expressed interest) and a plan to renovate, likely in tandem with Russia, the railway line running from Zimbabwe to the Mozambican coast.[20] This would create a Belarusian-Russian “corridor” for the two-way transport of goods. Furthermore, this would bring the associated infrastructure closer to the very same mineral deposits covered by the Lobito and Tazara Corridor projects. Before plans for the Belarusian-Russian corridor took shape, Russia had been attempting to influence public opinion in Angola. At the turn of 2024 and 2025, a group of Russian “political technologists” in Angola were responsible for the local media’s publication of content hostile to the Lobito project, e.g. comparing the agreement with Western partners to a “pact with the devil.”[21]

The Approach of States in the Region

The primary aim of the Corridor is to secure the supply chain to meet the EU and US demand for mineral resources. Although its creation is accompanied by the win-win narrative of cooperation with African countries, the Western partners are undoubtedly in the lead. At the same time, the region’s countries often lack sufficient insight and reflection into how to benefit from the Corridor’s development and ensure it serves as a genuine driver of well-considered economic integration.

Among Congolese experts, there is a clear belief that Angola will be the primary beneficiary of the programme, and that diverting goods from the region to Lobito will prove detrimental to the development of the deep-water port of Banana in the DRC[22]. Construction of the port, which will facilitate imports into the country[23], has been underway since 2022, with the UAE logistics giant DP World playing a key role. The port’s construction is also part of a Congolese-Chinese export infrastructure project for the very same deposits that the Lobito Corridor will transport. Known as the Banana Corridor, the project will provide a 3,300 km road link from the town of Sakania in the Congolese copper belt to the port of Banana. Completing the journey along this route, which runs parallel to the Benguela railway but lies entirely within DRC territory, is expected to take lorries four days.[24]

Angola does not consider the Angola–DRC–Zambia format, promoted by the Lobito Corridor’s creators, strategically optimal. For non-Corridor-related infrastructural projects in the region, it sees Botswana, for example, as a more reliable alternative to the problematic DRC. During a visit by that country’s President, Duma Boko, to Luanda in March 2026, discussions took place regarding the potential Botswanan acquisition of a 30% stake in the oil refinery in Lobito, which is under construction and not connected to the Corridor project. Zambia already owns 26% of the refinery. While the three Lobito Corridor nations would clearly benefit from jointly building a copper refinery—allowing them to share the profits from production at Angola’s first copper mine, opened in November 2025 in Tetelo—no government has proposed such a project. This indicates the somewhat artificial nature of the economic partnership of Angola and Zambia with the DRC.

Angolan and Zambian experts stress that the development of railway networks in the region only makes sense if they link the coasts of the Atlantic and Indian Oceans. This would create a continuous economic corridor, integrating the economies of Southern African countries. However, the very nature of the Lobito Corridor, positioned as a tool for the EU and the US to compete with China (which dominates the Tazara route), hinders, if not completely prevents, making use of this potential. Zambians are frustrated by the realisation that the Western initiators of the Lobito Corridor will never abandon the geopolitical dimension of this project. Zambia, through whose territory both the Lobito and Tazara routes are to pass, neither wants nor can afford to face the dilemma of choosing between being pro-Western or pro-Chinese. In an ideal world, the country could “force European-Chinese cooperation,”[25] but this is unrealistic. Consequently, the political reality constrains the corridor’s development potential.

There is a consensus in the region that with increased connectivity, inter-state trade could boom. Investing in better connections between the regions where specific goods are produced and sold is therefore desirable from a regional perspective. It is no coincidence, then, that Angola’s Minister of Transport, Ricardo Viegas D’Abreu, when discussing the corridor project at an economic conference in Luanda in December 2025, placed the greatest emphasis on the Caála Logistics Platform,[26] despite its marginal significance to both EU and US priorities and the project as a whole. If the Lobito Corridor raises expectations around tapping into the potential of non-mineral commercial connectivity, its geographic limitations may fuel frustration among regions and sectors that are left behind. For example, terrestrial orchids are widespread in Angola, and their tubers are used in Zambia to make chikanda, one of the country’s most popular dishes. Therefore, a huge market exists that could be exploited were it not for the distance and infrastructure problems. Meanwhile, record increases in maize production in Zambia (around 4 million tonnes in 2025) highlight its potential to meet the market needs of neighbouring countries such as Angola. Therefore, though the Lobito Corridor offers some very welcome improvements in regional non-mineral commercial connectivity, its priority status is detrimental to the development of other connections that would make more economic sense from the local perspective.

To unlock its true value, the countries involved not only need to deliver harmonisation of regulations on mobility and cross-border trade, but also a clear vision of the expected benefits, backed by the political determination of the region’s leaders to achieve them. Although they do consult and coordinate to some degree, for example, through the LCTTFA framework or at the presidential level (the summit of heads of state in July 2025), these are mostly reactive and belated measures. For example, following a meeting of transport ministers in Luanda in February 2026, a representative of the Congolese province of Haut-Katanga announced that, in collaboration with the World Bank, researchers from the universities of Lubumbashi and Kolwezi would conduct a study on the impact of the Lobito Corridor on the local economy. This step was intended to build on the Bank’s mission to Lubumbashi in September 2025, which aimed to identify the potential the Corridor offered the local population.[27] These measures, fundamental to establishing the DRC authorities’ approach to the project, should have been carried out at its earliest stages, before the decision to join was made. As it stands, they appear to be a mere—and belated—formality at best.

The DRC’s and Zambia’s attitude towards the Corridor project is best indicated by how it relates to the plans these countries have been developing in 2021–2022 to achieve self-sufficiency in battery production, and subsequently to enter the electromobility and clean energy sectors. These plans were motivated by the obvious need to avoid another “resource curse,” allowing the countries to capitalise on the global economic boom in a way that translates into improved living standards for their populations. Participation in the Lobito Corridor only partially fulfils the DRC’s and Zambia’s ambitions in this area. For example, these countries are increasing their share in the lithium-ion battery value chain, in part due to the construction of a hydrometallurgical plant at the COMIDE mine in the DRC’s Lualaba province. This facility will produce 30,000 tonnes of high-quality copper cathode and 5,000 tonnes of cobalt sulphate per year.[28] However, this capacity will not bring them any closer to their fundamental goal of becoming major global players in finished products. This ambition was previously championed by the Congolese Battery Council (CCB), established in 2022[29]. Yet, as the Lobito Corridor project gains momentum, the CCB has been sidelined, severely limiting the state's capacity to dictate its own trajectory in this area.

From a local perspective, the rhetoric regarding development opportunities stands in stark contrast to the reality of the political and economic situation. The DRC and Angola are among the most corrupt countries in the world (respectively ranked 163rd and 120th in Transparency International’s ranking[30]). The inherent characteristics of their economies may also pose an obstacle. In the DRC, state institutions are severely weakened by ongoing armed conflict (particularly in the Great Lakes region), whilst Angola is dominated by a corrupt and heavily subsidised state sector. The resulting environment is far from business-friendly. It is no coincidence that Angola ranked 177th[31] in the Doing Business ranking,[32] and even domestic Angolan entrepreneurs are not spared, often facing multi-year delays in receiving payment for completed work. The development of entire sectors of the economy is obstructed by the unwritten rule that businesses must obtain patronage from various factions of the ruling elite. Accustomed to reaping profits in dollars from oil exports—totalling US$450 billion during the peak growth period of 2002–2014[33]—the country has relied on this windfall to import necessary goods rather than developing domestic production and processing capabilities. There is a real risk that mineral exports via the Lobito Corridor will fall victim to this same mindset: “we will probably do the same as with oil: take the dollars to import whatever we can without producing anything.”[34]

A separate issue is the parasitic involvement of criminal groups in the region’s mineral economy. Truck drivers transporting goods between the Zambia–DRC border crossing and Kolwezi are subjected to a system of unofficial taxes, with bribes being demanded at numerous illegal checkpoints.[35] Any attempt to disrupt the revenue stream from this extortion risks provoking retaliation, such as sabotage.

The Project’s Uncertain Future

Progress on the project, which has accelerated since 2024, is impressive: the railway line in Angola is seeing month-on-month increases in transported cargo volumes. In 2025, the LAR consortium transported a total of 200,000 tonnes of cargo to and from the port of Lobito, with a record-breaking figure of 30,000 tonnes in December 2025. LAR currently states that its aim is for the line to reach an annual transport capacity of 1.5 million tonnes of minerals by 2027, and ultimately 4.6 million.[36] Work to upgrade the section linking the Angolan and DRC border to Kolwezi and Tenke is expected to begin by the end of 2026, while arrangements for extending this railway to the Zambian border should soon be finalised.

While the actual journey along the Angolan railway section takes only two days, the entire export process from DRC mines currently requires 30 to 35 days once storage in Kolwezi, administrative formalities, and port waiting times are factored in. In terms of speed, this timeframe is already competitive with regional alternatives, including rail or road routes through Tanzania, South Africa or Namibia. Ultimately, the target is to reduce the total round trip to 20 days, and current plans aim for 36 trains a week by 2027.

The Lobito Corridor’s share of trade in locally processed products is growing, thereby also improving the DRC and Angola’s contribution to global supply chains. In February 2026, the Kamoa-Kakula mine sold its first batch of locally refined copper,[37] and its majority owner has declared its readiness to transport between 120,000 and 240,000 tonnes of copper concentrate or blister copper anodes annually.[38]

State cooperation with small-scale producers is currently under review. For example, the Congolese state-owned company Entreprise Générale du Cobalt (EGC) partnered with Trafigura to complete its first cobalt sale on global markets in February 2026, following the DRC’s relaxation of export policies.[39] The scheme agreed upon is to be based on Trafigura supplying raw materials via the Lobito route to the EVelution Energy refinery in Arizona, which will cover around 40% of US demand.[40] Earlier, in November 2025, the Caála logistics platform was utilised to send an initial trial shipment of avocados to Rotterdam, testing the logistics and procedures ahead of the route’s planned commercial launch.

However, the project’s successes to date do not guarantee its ultimate success. Since the start of Donald Trump’s second term, the US approach to its presence in Africa has changed significantly, particularly regarding its humanitarian and development aspects. Although from the outset the Lobito Corridor project has primarily focused on minerals, it was also situated within a broader development framework. USAID, which Trump abolished, played a significant role in implementing environmental elements; in March 2024, it allocated $235 million to support Angola’s National Development Programme, as well as additional funds for a programme to empower women in agriculture and combat malaria.[41] During this period, the then-head of USAID, Samantha Power, was one of the “faces” of US engagement in the Lobito Corridor. The US-Angolan agreement, concluded under the PGII shortly afterwards, was also based on development activities across Angola (worth $1.3 billion), including the construction of two solar power plants, 186 bridges and the expansion of shortwave infrastructure to cover 95% of the population.[42] Currently, the US approach to partnerships and resources is seeing drastic changes, exemplified by the intervention in Venezuela, a move explicitly framed as an effort to secure access to the country’s oil reserves. In Africa, a prime example of this shift was the proposal for a US-Congolese “minerals for security” agreement, put forward in early 2025.[43] Facing defeat at the hands of the Rwanda-backed M23, the DRC initiated this partnership from a position of weakness. By assuming the role of a client state, the DRC sought to trade access to its strategic resources for immediate US security assistance and promises of diplomatic or military support. This strategy was formalised in the Congolese-American agreement of 4 December 2025. Under its terms, Congolese state-owned companies are committed to channelling 50% of copper, 30% of zinc and 90% of cobalt through the port of Lobito over the next five years.[44] These arrangements present a challenge to the anticipated launch of the Congolese Banana Corridor, which will offer a faster four-day mine-to-port transit. This local alternative may prompt the DRC’s business community and its authorities to de-prioritise Lobito as a route for strategic exports.

The current US administration’s tactic of exploiting African partners’ vulnerable political or security situations to secure access to raw materials leaves little space for their agency or ambitions.[45] Another alarm bell for African states in this regard was Secretary of State Marco Rubio’s speech in Munich on 14 February 2026. Rubio argued that colonial empires could serve as a template for contemporary US and European relations with the Global South, including economic exploitation.[46] In response, mistrust of US strategic intentions intensified across Africa, particularly concerning mineral partnerships. By the end of February, this scepticism had spilled over into other areas of cooperation, leading to countries such as Zambia and Zimbabwe refusing to sign bilateral agreements with the US on healthcare. In doing so, they cited the need to defend national interests, fearing that aid would be contingent on providing mineral access, and that cooperation would grant the US uncontrolled access to personal data.[47]

At the same time, African countries are becoming increasingly aware of their leverage over stronger external partners, particularly when they possess advantages such as a high concentration of key mineral resources. In a bid to drive up global market prices,[48] the DRC suspended cobalt exports for 10 months in 2025. The country’s finance minister, Doudou Fwamba, justified the move as necessary to strengthen “national sovereignty over raw materials.”[49] To that end, the country is to create a national cobalt reserve. Zimbabwe, home to Africa’s largest lithium deposits, has also followed this path. On 25 February 2026, the country announced an immediate suspension of exports of raw minerals and lithium concentrate, accelerating a move that was previously not expected until 2027.[50] The move was intended to pressure its major partners—particularly from China, which relies on Zimbabwe for 19% of lithium imports—after many failed to deliver on promises to develop processing facilities.[51] The country then announced a partial resumption of exports, but only for partners who provide written commitments to open lithium sulphate production facilities in Zimbabwe by 1 January 2027. Similarly, in February this year, Ghana announced a plan to process all minerals mined on its territory locally by 2030.[52] Furthermore, the success of the Dangote refinery in Nigeria—privately funded by the country’s wealthiest businessman —in securing regional fuel supplies during the Middle East crisis has changed the perspective of many African leaders. It has demonstrated the value of prioritising domestic industry over the dominance of foreign giants, setting the stage for an inevitable clash between US interests and African agency.

The Lobito project is hardly immune to unexpected geopolitical upheavals. The conflict between the US, Israel, and Iran has disrupted the global market for sulphur, essential to copper refining. Maintaining continuous supplies of this raw material from the port of Lobito to Kolwezi is critical, but given that the Middle East accounts for 24% of global sulphur production and that it transits the Strait of Hormuz, there is an acute supply continuity risk. By the start of March, this vulnerability was clear: reserves were projected to last only a few weeks amidst soaring global prices.[53]

The EU’S Role

The perceived success of the project depends on a diverse set of local, pan-African, and global influences, both for the key US and EU partners and in the eyes of African nations. In 2026, the Lobito Corridor project stands at a crossroads, caught between contradicting philosophies. Despite its clear focus on raw materials, it is anchored in a development-cooperation that the West is moving away from.

The atmosphere surrounding the Corridor is also shaped by the changing nature of global competition for resources. It is no longer only the countries of the Global North that are competing for access, but also African nations—aware of the threats this competition poses to them—are taking countermeasures and demonstrating increasing agency in shaping resource policies and independent ability to influence global markets. These trends create a climate of uncertainty regarding future cooperation on the Lobito Corridor, such as the construction of the new Zambia–Angola railway section.

Therefore, in the context of the US’s shifting stance—embodied by the contrast between the “development-oriented” agreement with Angola in May 2024 and the “imperial” one with the DRC in December 2025—it is essential for the EU to maintain its credibility. By consistently offering and delivering a win-win strategy, the EU could thus become the partner of choice for the region’s countries.

To this end, the EU should—in addition to the measures already being implemented to strengthen local value chains in the agricultural trade sector—place greater emphasis on developing passenger transport within the Lobito Corridor.

Whilst emphasising the development aspects it supports, the EU’s task is also to build the image of the Lobito Corridor as a European-American initiative, rather than an American-European one, as it is currently perceived.

More broadly, the EU should clearly encourage the development of local processing industries in raw material-producing countries, to generate stability and resilience in the long term.

Therefore, the EU’s policy to counterbalance Chinese influence must not come at the expense of the development potential of the region’s countries. For instance, the EU could engage with the Banana Corridor project in the DRC to ensure it benefits local communities in the future, as with the Lobito Corridor approach.

For the EU, successful projects linked to the Lobito Corridor—which benefit partner countries and local communities—should serve as a benchmark for future Global Gateway initiatives. By establishing this standard, the EU can present itself to the Global South as offering a high-quality alternative to the infrastructure plans of non-European countries.

[1] C. Mfula, O. Kumwenda-Mtambo, “Zambia seeking global investors to help triple copper output by 2031,” Reuters, www.reuters.com.

[2] “Cobalt facts,” Government of Canada, https://natural-resources.canada.ca.

[3] In 2023, the DFC committed a total of $8.1 billion to projects under the PGII.

[4] J. Pacquet, “US and EU join forces on rail corridor in play for African minerals,” The Africa Report, 14 September 2023, https://www.theafricareport.com.

[5] In 1973, prior to independence, domestic freight accounted for approximately 44% of rail freight traffic in Angola, but this share gradually declined to minimal levels.

[6] In February 2026, a new format was established on this basis: the Forum on Engagement in Geostrategic Resources (FORGE).

[7] “Joint Statement from the United States and the European Union on Support for Angola, Zambia and the Democratic Republic of the Congo’s commitment to Further Develop the Lobito Corridor and the U.S.-EU Launch of a Greenfield Rail Line Feasibility Study,” The White House, 9 September 2023, https://bidenwhitehouse.archives.gov.

[8] “Corridor Background,” Lobito Corridor Investment Promotion Authority, https://www.lobitocorridor.org/history-background.

[9] M. Hill, “The US and EU Plan $1 Billion-Plus Africa Rail Link for Key Minerals,” Bloomberg, 1 November 2023, https://www.bloomberg.com.

[10] R. Luabeya, “Lobito Corridor: Rail works on DRC section expected to begin in late 2026,” Bankable, 9 February 2026, https://bankable.africa.

[11] “FACT SHEET: Partnership for Global Infrastructure and Investment in the Lobito Trans-Africa Corridor,” The White House, 3 December 2024, https://bidenwhitehouse.archives.gov.

[12] “EU-Angola partnership advanced through major investments in the Lobito Corridor,” Directorate-General for International Partnerships, 9 October 2025, http://global-gateway-forum.ec.europa.eu/news.

[13] Helaina Matza, the US PGII coordinator, described it as the most important transport infrastructure that the US has helped to build in Africa in a generation.

[14] “Lobito Corridor: What It Is & Why It Matters,” Lobito Corridor Investment Promotion Authority, January 2024, www.lobitocorridor.org, p. 10.

[15] W. Cloves, “Zijin’s Congo Lithium Mine Set to Be Among World’s Biggest,” Bloomberg, 24 March 2026, https://www.bloomberg.com/news.

[16] “Lobito Corridor to Enhance Freight Capacity with 275 New Wagons from South Africa’s Galison Manufacturing,” Lobito Corridor Investment Promotion Authority, 30 May 2024, https://www.lobitocorridor.org.

[17] Chinese announcements had promised up to 20 million tonnes of goods and 4 million passengers per year, but only a fraction of these targets were actually achieved.

[18] “Duelling Rail Projects Hint at Intensifying Contest for Africa’s Critical Minerals,” Lobito Corridor Investment Promotion Authority, 30 April 2024, https://www.lobitocorridor.org.

[19] “Evaluating the Lobito Corridor: The Future of Cobalt in Sub-Saharan Africa,” EHS Africa Logistics, 11 November 2024, https://ehsafricalogistics.com.

[20] “Belarus offering Zimbabwe to join construction of seaport in Mozambique,” SB, 23 February 2026, https://www.sb.by.

[21] M. Jevstafjeva, I. Barabanov, L. Prazeres, “Inside the alleged Russian operation to trigger anti-government protests in Angola,” BBC, 24 March 2026, https://www.bbc.com/news.

[22] Interview with Danny Kambo in Kinshasa, December 2025.

[23] At present, goods destined for Kinshasa mostly arrive through the Point-Noire port in neighbouring Congo-Brazzaville, which is time-consuming and costly.

[24] “DRC on Track to Complete 3,300 km Sakania-Banana Corridor by 2027, ACGT Says,” Bankable, 6 November 2025, https://bankable.africa.

[25] Interview with a Zambian government official, December 2025.

[26] “Issue 4 | Economy 100 MAKAS | 1 December 2025,” Radio MFM, 1 December 2025, https://www.youtube.com.

[27] C. Muamba, “Luanda: a high-level tripartite the DRC, Zambia and Angola with the World Bank on the Lobito corridor,” Actualite.cd, 4 February 2026, https://actualite.cd.

[28] “DRC advances mineral beneficiation with SEZs, new refineries,” Energy Capital Power, 9 December 2025, https://energycapitalpower.com.

[29] J. Czerep, “The DRC’s prospects for entering the global market for electric vehicle batteries,” PISM Bulletin, no. 19 (2138), 2 March 2023, www.pism.pl.

[30] “Corruption Perception Index 2025,” Transparency International, https://www.transparency.org/en/cpi/2025.

[31] For comparison, Botswana ranked 87th and South Africa 84th.

[32] “Latest Doing Business ranking,” World Bank, 2019.

[33] “Angola from boom to bust – to breaking point,” CMI Chr. Michelsen Institute, 8 April 2016, http://www.cmi.no.

[34] Author’s interview with Carlos Rosado de Carvalho, Luanda, December 2025.

[35] “The Lobito Corridor: Economic Opportunity and Investment Risk,” Alma, 3 March 2026, https://www.alma-risk.com.

[36] A. Botha, “Angola: Lobito Corridor Targets 1.5M Tonnes of Mineral Transport by 2027,” Further Africa, 8 April 2025, https://furtherafrica.com.

[37] “Trafigura, Aurubis and Kamoa Copper Complete First Sale of Low-Carbon Refined Copper via the Lobito Atlantic Railway,” Lobito Atlantic Railway, 19 February 2026, https://www.lobitoatlantic.com.

[38] “Ivanhoe Mines’ Kamoa-Kakula Signs Term Sheet to Export Copper Along the Lobito Atlantic Railway Corridor,” Ivanhoe Mines, 7 February 2024, https://www.ivanhoemines.com/news-stories.

[39] “EGC and Trafigura ship copper and cobalt to global markets via the Lobito Atlantic Railway,” Lobito Atlantic Railway, 9 February 2026, https://www.lobitoatlantic.com.

[40] “Entreprise Générale du Cobalt, EVelution Energy and Trafigura sign MOU to establish direct U.S.–DRC cobalt supply chain,” Trafigura, 13 May 2026, https://www.trafigura.com/news-and-insights/.

[41] “USAID Administrator Announces New Investments Along the Lobito Corridor,” Lobito Corridor Investment Promotion Authority, 30 May 2024, https://www.lobitocorridor.org.

[42] “Partnership for Global Infrastructure and Investment (PGI) Celebrates Signing of Finance Agreements for Republic of Angola Projects,” U.S. Department of State, 7 May 2024, https://www.state.gov.

[43] J. Czerep, “Rwandan-Congolese peace under US auspices,” PISM Bulletin, no. 67 (2568), 3 July 2025, www.pism.pl.

[44] I. Linge, P. Mukoko, “Mota-Engil Poised for DRC Rail Concession as US and Kinshasa Cement Lobito Strategy,” EcoFin Agency, 11 December 2025, https://www.ecofinagency.com/news-infrastructures.

[45] For example, no Sub-Saharan African country has been invited to the Board of Peace.

[46] “Secretary of State Marco Rubio at the Munich Security Conference,” U.S. Department of State, 14 February 2026, https://www.state.gov.

[47] “Zambia rejects Trump’s $1bn health funding plan linked to data access,” TRT Afrika, 26 February 2026, https://www.trtafrika.com.

[48] Prices rose from $22,000 to $54,000 per tonne.

[49] “Democratic Republic of Congo resumes cobalt exports after 10-month ban,” Africa News, 23 December 2025, https://www.africanews.com.

[50] “Zimbabwe imposes ban on exports of all raw minerals and lithium concentrate,” Al Jazeera, 25 February 2026, https://www.aljazeera.com.

[51] These partners include Sinomine and Yahua. An exception to this was Huayou, which in February 2026 launched Africa’s first such plant, built at a cost of $400 million.

[52] “Ghana to process all minerals by 2030,” Africa Briefing, 26 February 2026, https://africabriefing.com.

[53] D. Duan, P. Desai, T. Daly, “Gulf disruption squeezes Indonesia nickel makers’ sulphur supply,” Reuters, 6 March 2026, https://www.reuters.com.